tuxumino

Purrfect

welp early retirement is off the table")

yeah it's starting to look like I'll have to work a few more years to bump up the pension to cover what stocks lost.

welp early retirement is off the table

Do you not have a Roth 401k option?

I'd heard between traditional/Roth and 401K/IRA, do one of each -- so if you have a Roth IRA (as I do), then opt for the traditional 401k or the inverse (traditional IRA/Roth 401).

Don't remember the details anymore but the reasoning made sense at the time.

Posted this in another thread but thought I'd post here also.

Even us retired folks need to keep in mind that 20 percent or so of money in our non Roth IRAs goes to Uncle Sam.

We'll be working on mitigating that between 65 and 70 when we start collecting Social Security by using those 5 years to draw down our IRAs while I'm in a lower tax bracket.

Once we collect SS combined will be +$80,000 +/-.

Not starting until age 65 as we are trying to maintain our income at a level that still qualifies us for a Health Care subsidy.

Before that subsidy we were paying 17k/yr, it would, obviously, be much much higher today.

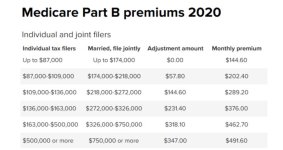

Also look at the costs of Medicare. I met someone who'll turn 65 soon. And she told me that Medicare (Part B?) will cost her $850 out of her Sosh Sec.!

She said every month.

Hard to believe, bc she looks very healthy for a senior. But she might have diabetes and hypertension and we know how insidious the former can be on the human body as a person ages.

$850.00 per annum? $71.00 per month hopefully won't negatively impact her too much.

So I could retire in April but if I wait a month I get an extra .25 %.

Sucking part about IRA --> Roth IRA backdoor is that even if you deposit in to IRA and immediately convert to Roth IRA, it's counted as 6k withdrawl or someting At least in my taxes it's extra 1k something in taxes I owe.

I am afraid my retirement is being tossed out the window without a mask.

Did you use TurboTax? I had the same issue with their software.

She said every month.

Hard to believe, bc she looks very healthy for a senior. But she might have diabetes and hypertension and we know how insidious the former can be on the human body as a person ages.

Bump to the front...where should us youngers be looking to put our money in once the parabola hits the base?